Dow Jones above 30’000 for the first time

Dow Jones above 30’000 for the first time

What a day! Nasdaq is above 12’000, and S&P 500, Russel 2000 and the Dow closed at record levels. Meanwhile the US sees another spike in new COVID-19 cases. It is as well remarkable that this surge was not accompanied by large volumes. There is little euphoria among retail investors and UHNWI investors have net reduced their equity allocation this year.

Strategists and asset manager are bullish according to BofA latest survey. The short sellers at the New York stock exchange are below 1.5%. There is a lot of complacency and no fear.

Fig. 1: Dow Jones is above 30’000

A pullback to digest the recent rally has not happened so far, by the contrary, we have seen a sector rotation. This new record levels happened without the support of the FANG+ stocks. The Russel 2000 went up 20% over the last three weeks!

The reasons for this surge: Reduced political uncertainty moved stocks up. The hope for more fiscal stimulus and monetization of the public debt by selecting Mrs. Yellen, former fed chair, as US Treasury Secretary might be another reason. The announcement of a 3rd effective vaccine against Covid-19 at the beginning of the week as well created hope of a fast reopening economy. Although even in the best case less then two billion people might get vaccinated in H1 2021, which basically means it will not be over in 2021, but nobody cares about it right now.

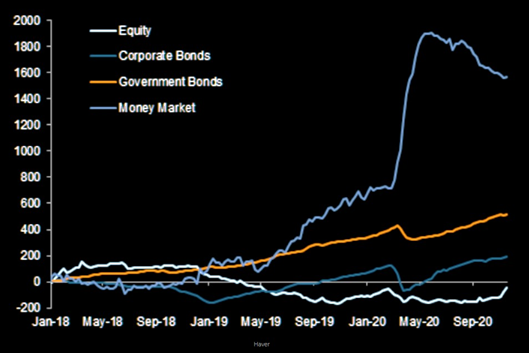

Fig. 2: Inflow into equites over the last 2 years is still net slightly negative

Fig. 3: Risk-on sends gold down sharply

Gold on the other hand sold off to its 200-day average. If it stopped falling this would be a classical correction within a bull market. It must be seen if we see a mean reversion from this level. The main ingredients for the gold rally are still intact. Rising budget deficit, strong monetary and fiscal stimulus, negative yielding bonds, and political uncertainty are just some of the reasons why the gold price might stabilize and continue to go up again.

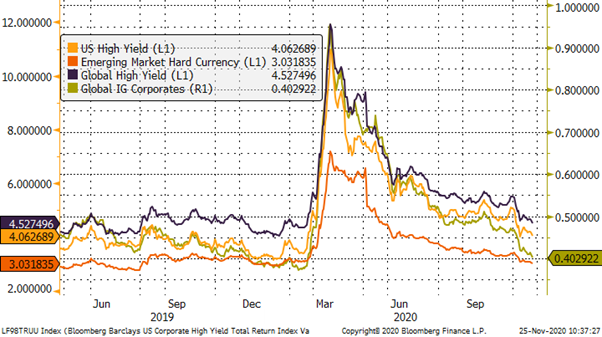

The search for yield is ongoing. Most high-quality bonds are either yielding nominal negative or are returning a negative real yield after inflation. Global corporate non-investment grade bonds have seen more inflows and yields are now at levels between 3-4.6%. This means one gets not compensated for the risk these bonds have. But the TINA (there is no alternative) argument holds not only true for equites but also for bond investors.

Fig. 4: Global Corporate bonds have continued to surge

For the foreseeable future we expect yields to stay at low levels, but we must as well expect a surge in defaults over the coming months. However, we expect that due to the zombification (i.e. companies which are held artificially alive due to very cheap refinancing opportunities) the cleanup process will take more time than rating agencies estimate. In the Russel 2000 index roughly 20% of all listed companies are so called zombies with a lot of outstanding debt.

What comes next? The overdue equity market correction has not happened. It might well be that US markets will rise like 4 years ago into the beginning of next year. However, they cannot go up forever and we expect a correction within a bull market over the coming months.

Fig. 5: Over the last three months Nasdaq 100 has most equity markets

Over the last three months as expected Asia and Latin America did outperform Europe and the US. The sector rotation in the US resulted in a 18% surge of the Russel 2000 while the Nasdaq 100 only went up 3%. We expect that all three areas will continue to perform well over the coming weeks. Europe had a strong catch up rally, but we would expect based on weak recent economic indicators (PMIs or IFO) that this will come to end.

Corporate non-investment grade bonds (i.e. US high yields and Asian corporates) would if we were right with our positive equity outlook deliver the coupon and should on average not suffer from spread widening. Any bad news can however trigger selloffs as a correction is overdue, but momentum and liquidity speak against it in the short run. If, however, we were to see a pullback, that could offer an opportunity to enter the market.

Disclaimer: This Blackfort Insights (hereafter «BI») is provided for information purposes only. This document was produced by Blackfort Capital AG (hereafter «BF») with the greatest care and to the best of its knowledge and belief. Although information and data contained in this document originate from sources that are deemed to be reliable, no guarantee is offered regarding the accuracy or completeness. Therefore, BF does not accept any liability for losses that might occur using this information. BI does not purport to contain all the information that may be required to evaluate all the factors that would be relevant for entering into any transaction and anyone hereof should conduct their own investigation and analysis. In addition, the BI includes certain projections and forward-looking statements. Such projections and forward-looking statements are subject to significant business, economic and competitive uncertainties and contingencies, many of which are beyond the control. Accordingly, there can be no assurance that such projections and forward-looking statements will be actualized. The real results may vary from the anticipated results and such variations may be material. No representations or warranties are made as to the accuracy, or reasonableness of such assumptions, or the projections, or forward-looking statements based thereon. This document is expressly not intended for persons who, due to their nationality or place of residence, are not permitted to access such information under local law. It may not be reproduced either in part or in full without the written permission of BF.

© Blackfort Capital AG. All Rights reserved.

Media about us:

-

-

Capital for The Energy-efficient Renovation of Swiss Homes

Uncorrelated earnings in Swiss Francs and more capital for the energetic refurbishment of Swiss houses – In the interview Wanja Eichl, Managing Partner, explains why Blackfort launches the new Swiss Real Estate Debt Fund. Please check it out via the following INTERVIEW Blackfort Swiss Real Estate Debt_e

-

More Capital for The Energetic Refurbishment of Swiss Real Estate

Contact us

Blackfort Capital AG Blackfort Schweiz AG

Talstrasse 61, 8001 Zurich Prime Tower, 8005 Zurich

Tel. +41 44 585 7878 Tel. +41 44 442 3202